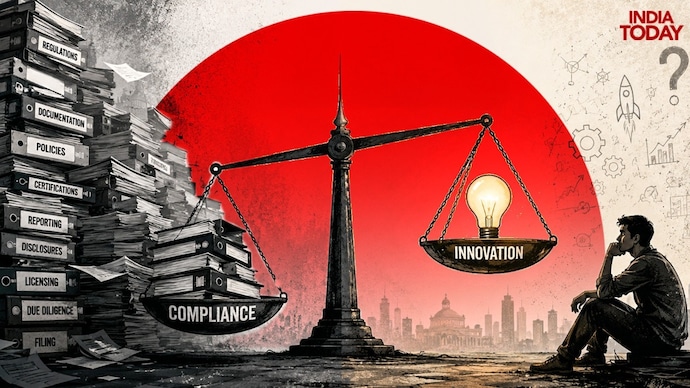

Did India's compliance push cost it the next investment boom?

India has improved ease of doing business over the past decade, but is that enough in a world increasingly shaped by AI, semiconductors and deep technology?

For much of the last decade, the government has focused on making India a cleaner, more transparent and more compliant economy.

The rollout of GST, the Insolvency and Bankruptcy Code, tighter compliance requirements and a broader push towards formalisation transformed the way businesses operated. The expectation was that stronger institutions, greater transparency and improvements in the ease of doing business would make India a more attractive destination for investment.

Yet while India was focused on formalisation, compliance and improving the investment climate, a different race was unfolding around the world, one that was increasingly attracting global investors.

Countries such as the United States, Taiwan, China and South Korea were pouring resources into artificial intelligence, semiconductors, advanced manufacturing and deep technology.

Taiwan has established itself as the nerve centre of the global chip industry. South Korea emerged as a major beneficiary of the AI and memory-chip boom. The United States attracted unprecedented investment into AI infrastructure and computing.

The consequences are increasingly visible in capital flows. Despite being the world's fastest-growing major economy, India has struggled to attract foreign capital at the pace many expected. Why that gap persists, despite strong economic growth, is a question we explored in detail in our earlier analysis, "India's economy is booming. So why are foreign investors looking away?"

Which brings us to a broader question: Has India's focus on compliance, formalisation and ease of doing business been matched by a similar push into innovation, research and strategic technologies?

The answer, according to economists, policymakers and the data, is at best complicated.

The debate has gained traction among many investors and entrepreneurs, many of whom argue that while many of the countries mentioned above have built capabilities in AI, semiconductors and manufacturing, India concentrated on compliance, formalisation and regulatory reform.

Some economists believe there is merit to at least part of that argument.

"Since 2014, India has prioritised balance-sheet repair, regulatory tightening and tax and corporate compliance to reduce execution risks and improve investor confidence," said Manoranjan Sharma, Chief Economist at Infomerics Ratings.

But Sharma also points to what he sees as a missing piece.

"Modest public R&D spending, modest patent approvals, and limited support for deep-tech and hardware ventures were headwinds. China, South Korea and several ASEAN economies invested heavily in applied research, AI infrastructure and semiconductor capacity," he said.

The data appears to support this concern.

According to the latest government data available, India's Gross Expenditure on Research and Development (GERD) stood at 0.64% of GDP in 2020-21 and has largely remained in the 0.6-0.7% range for years.

In contrast, South Korea spends more than 5% of its GDP on research and development, while the United States spends over 3% and China more than 2.5%, according to international R&D data.

A recent NITI Aayog report on the ease of doing research and development highlighted funding constraints, talent shortages and weak industry participation as major challenges facing India's innovation ecosystem. A NITI-backed survey also found that a majority of researchers said industry rarely supports research financially.

For Sharma, these shortcomings help explain why the first wave of global investment into semiconductors and AI largely flowed elsewhere.

"India lacked the first-mover advantage in semiconductors and AI computing as strategic national capabilities. Consequently, the first wave of global investments flowed to the USA, Taiwan, South Korea, Vietnam and parts of the Gulf," he said.

BUT IS COMPLIANCE REALLY THE PROBLEM?

Not everyone agrees that India's focus on compliance is responsible for foreign investors looking elsewhere.

Dr VK Vijayakumar, Chief Investment Strategist at Geojit Investments, argues that the debate often misses a more important factor.

"Global capital pursues returns, not growth," he said.

According to Vijayakumar, foreign investors have not necessarily turned away from India because of compliance requirements or regulatory processes. Instead, they have been chasing extraordinary earnings growth generated by the AI boom.

During the past two years, a handful of companies have emerged as the biggest beneficiaries of the global AI race. Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics and SK Hynix have seen investors flock to their stocks as demand for AI chips and computing infrastructure surged.

"It is a fact that India is not present in the semiconductor segment, which is dominated by South Korea, Taiwan and the USA," Vijayakumar said.

Recent market trends appear to support his argument.

Earlier this month, India slipped from fifth to seventh place in global stock market rankings after being overtaken by Taiwan and South Korea. The rally in those markets has been driven largely by semiconductor and AI-linked companies.

According to Reuters, foreign investors have pulled billions of dollars from Indian equities this year while increasing exposure to Taiwan and South Korea, where markets offer direct participation in the AI and semiconductor boom.

To be sure, foreign investors have often pointed to taxation, compliance requirements and regulatory complexity as concerns, prompting policymakers to roll out measures aimed at improving the investment climate.

But Vijayakumar believes those factors tell only part of the story. As AI reshapes global capital flows, investors are increasingly gravitating towards markets offering direct exposure to the technologies generating the world's fastest earnings growth.

WHAT THE DATA SHOWS

The evidence also suggests that India is not an innovation laggard.

According to the World Intellectual Property Organisation's Global Innovation Index 2025, India ranks 38th among 139 economies, up from 48th in 2020. It also remains the highest-ranked lower-middle-income economy.

India has developed a vibrant startup ecosystem, become a major exporter of IT and digital services and emerged as one of the world's largest digital economies.

The problem, however, may not be innovation itself.

It may be the type of innovation.

India has built successful software, fintech and digital-services companies. But it has yet to produce globally dominant players in semiconductors, advanced computing, AI hardware or other deep-tech sectors that currently sit at the centre of global capital flows.

That distinction is important.

The world's biggest investment story today is not software alone. It is the infrastructure powering artificial intelligence — chips, data centres, advanced computing and semiconductor manufacturing.

These are precisely the sectors where countries such as Taiwan, South Korea and the United States built advantages years ago.

THE BIGGER QUESTION

The debate, then, is not really about whether compliance was a mistake. Most economists agree that stronger institutions, greater transparency and better governance were necessary for India's long-term development.

The real question is whether compliance and formalisation were accompanied by enough investment in research, technology and strategic industries.

The government's own policy institutions appear to believe more needs to be done. NITI Aayog has called for higher R&D spending, stronger industry participation in research, better talent development and a more innovation-friendly ecosystem.

The challenge for India may therefore be different from the one it faced a decade ago.

The last ten years were largely about fixing the system. The next ten, according to economists, should focus on building the technologies and industries that attract global capital in an AI-driven world.

For much of the last decade, the government has focused on making India a cleaner, more transparent and more compliant economy.

The rollout of GST, the Insolvency and Bankruptcy Code, tighter compliance requirements and a broader push towards formalisation transformed the way businesses operated. The expectation was that stronger institutions, greater transparency and improvements in the ease of doing business would make India a more attractive destination for investment.

Yet while India was focused on formalisation, compliance and improving the investment climate, a different race was unfolding around the world, one that was increasingly attracting global investors.

Countries such as the United States, Taiwan, China and South Korea were pouring resources into artificial intelligence, semiconductors, advanced manufacturing and deep technology.

Taiwan has established itself as the nerve centre of the global chip industry. South Korea emerged as a major beneficiary of the AI and memory-chip boom. The United States attracted unprecedented investment into AI infrastructure and computing.

The consequences are increasingly visible in capital flows. Despite being the world's fastest-growing major economy, India has struggled to attract foreign capital at the pace many expected. Why that gap persists, despite strong economic growth, is a question we explored in detail in our earlier analysis, "India's economy is booming. So why are foreign investors looking away?"

Which brings us to a broader question: Has India's focus on compliance, formalisation and ease of doing business been matched by a similar push into innovation, research and strategic technologies?

The answer, according to economists, policymakers and the data, is at best complicated.

The debate has gained traction among many investors and entrepreneurs, many of whom argue that while many of the countries mentioned above have built capabilities in AI, semiconductors and manufacturing, India concentrated on compliance, formalisation and regulatory reform.

Some economists believe there is merit to at least part of that argument.

"Since 2014, India has prioritised balance-sheet repair, regulatory tightening and tax and corporate compliance to reduce execution risks and improve investor confidence," said Manoranjan Sharma, Chief Economist at Infomerics Ratings.

But Sharma also points to what he sees as a missing piece.

"Modest public R&D spending, modest patent approvals, and limited support for deep-tech and hardware ventures were headwinds. China, South Korea and several ASEAN economies invested heavily in applied research, AI infrastructure and semiconductor capacity," he said.

The data appears to support this concern.

According to the latest government data available, India's Gross Expenditure on Research and Development (GERD) stood at 0.64% of GDP in 2020-21 and has largely remained in the 0.6-0.7% range for years.

In contrast, South Korea spends more than 5% of its GDP on research and development, while the United States spends over 3% and China more than 2.5%, according to international R&D data.

A recent NITI Aayog report on the ease of doing research and development highlighted funding constraints, talent shortages and weak industry participation as major challenges facing India's innovation ecosystem. A NITI-backed survey also found that a majority of researchers said industry rarely supports research financially.

For Sharma, these shortcomings help explain why the first wave of global investment into semiconductors and AI largely flowed elsewhere.

"India lacked the first-mover advantage in semiconductors and AI computing as strategic national capabilities. Consequently, the first wave of global investments flowed to the USA, Taiwan, South Korea, Vietnam and parts of the Gulf," he said.

BUT IS COMPLIANCE REALLY THE PROBLEM?

Not everyone agrees that India's focus on compliance is responsible for foreign investors looking elsewhere.

Dr VK Vijayakumar, Chief Investment Strategist at Geojit Investments, argues that the debate often misses a more important factor.

"Global capital pursues returns, not growth," he said.

According to Vijayakumar, foreign investors have not necessarily turned away from India because of compliance requirements or regulatory processes. Instead, they have been chasing extraordinary earnings growth generated by the AI boom.

During the past two years, a handful of companies have emerged as the biggest beneficiaries of the global AI race. Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics and SK Hynix have seen investors flock to their stocks as demand for AI chips and computing infrastructure surged.

"It is a fact that India is not present in the semiconductor segment, which is dominated by South Korea, Taiwan and the USA," Vijayakumar said.

Recent market trends appear to support his argument.

Earlier this month, India slipped from fifth to seventh place in global stock market rankings after being overtaken by Taiwan and South Korea. The rally in those markets has been driven largely by semiconductor and AI-linked companies.

According to Reuters, foreign investors have pulled billions of dollars from Indian equities this year while increasing exposure to Taiwan and South Korea, where markets offer direct participation in the AI and semiconductor boom.

To be sure, foreign investors have often pointed to taxation, compliance requirements and regulatory complexity as concerns, prompting policymakers to roll out measures aimed at improving the investment climate.

But Vijayakumar believes those factors tell only part of the story. As AI reshapes global capital flows, investors are increasingly gravitating towards markets offering direct exposure to the technologies generating the world's fastest earnings growth.

WHAT THE DATA SHOWS

The evidence also suggests that India is not an innovation laggard.

According to the World Intellectual Property Organisation's Global Innovation Index 2025, India ranks 38th among 139 economies, up from 48th in 2020. It also remains the highest-ranked lower-middle-income economy.

India has developed a vibrant startup ecosystem, become a major exporter of IT and digital services and emerged as one of the world's largest digital economies.

The problem, however, may not be innovation itself.

It may be the type of innovation.

India has built successful software, fintech and digital-services companies. But it has yet to produce globally dominant players in semiconductors, advanced computing, AI hardware or other deep-tech sectors that currently sit at the centre of global capital flows.

That distinction is important.

The world's biggest investment story today is not software alone. It is the infrastructure powering artificial intelligence — chips, data centres, advanced computing and semiconductor manufacturing.

These are precisely the sectors where countries such as Taiwan, South Korea and the United States built advantages years ago.

THE BIGGER QUESTION

The debate, then, is not really about whether compliance was a mistake. Most economists agree that stronger institutions, greater transparency and better governance were necessary for India's long-term development.

The real question is whether compliance and formalisation were accompanied by enough investment in research, technology and strategic industries.

The government's own policy institutions appear to believe more needs to be done. NITI Aayog has called for higher R&D spending, stronger industry participation in research, better talent development and a more innovation-friendly ecosystem.

The challenge for India may therefore be different from the one it faced a decade ago.

The last ten years were largely about fixing the system. The next ten, according to economists, should focus on building the technologies and industries that attract global capital in an AI-driven world.