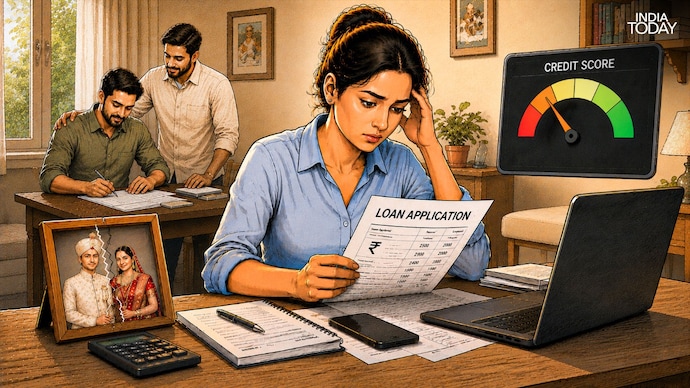

A joint loan, a separation and a damaged credit score: Her story is a warning

'She' wasn't the one who defaulted, yet her loan application was affected. 'He' never borrowed the money, yet he had to repay the debt. These two real-life stories reveal the hidden risks of saying 'yes' to someone else's loan. Could the same happen to you?

"I had done everything right. So why was the bank treating me like a risky borrower?"

That question still haunts a friend of mine, a university professor who wishes to remain anonymous.

For years, she had been the kind of borrower banks love. Every credit card bill was paid on time. Every loan repayment was made without fail. She believed, like most of us do, that a good credit score was simply a reflection of personal financial discipline.

Then came a rude shock.

After separating from her husband, she decided to move on with life and applied for a personal loan. With a steady income and an impeccable repayment record, she expected the approval process to be routine.

It wasn't.

Banks either rejected her application or offered her a loan amount far below what she was eligible for.

Confused, she dug deeper.

That's when she discovered that her former husband had defaulted on multiple EMIs of the home loan they had once taken jointly.

Those missed payments on the joint loan had quietly affected her credit report, dragging down her credit score as well.

She had never missed an EMI or delayed a credit card payment herself. Yet her creditworthiness had taken a hit because of someone else's financial behaviour.

After months of discussions, paperwork and persuasion, she eventually secured a loan, but for a much smaller amount than she had originally sought, despite earning well enough to qualify for more.

Her experience reveals one of the least understood truths about borrowing: your credit score isn't always shaped only by your own financial discipline. Sometimes, it's shaped by someone else's decisions too.

YOUR SIGNATURE CARRIES MORE WEIGHT THAN YOU THINK

Many people believe that a credit score is influenced only by loans they personally borrow and repay.

Not quite.

According to Jyoti Prakash Gadia, Managing Director, Resurgent India Limited, becoming a co-borrower or guarantor legally ties your financial reputation to another person's repayment behaviour.

"It is often thought that an individual's credit score depends solely on one's loans, credit card usage and repayment behaviour. But that is not entirely true. If an individual acts as a co-borrower or guarantor to someone else's loan, even those loans may affect the individual's credit profile. Any default recorded against an individual can impact his or her future borrowing capacity."

In other words, your spotless repayment history may not be enough if you're legally connected to someone else's loan.

HELPING SOMEONE CAN TURN INTO A FINANCIAL LIABILITY

Few people think twice before signing loan documents for a loved one.

Parents become co-applicants on education loans. Couples jointly buy homes. Siblings stand guarantee for business loans. Friends step in during difficult times.

The intention is usually to help.

The legal consequences, however, can last much longer than the circumstances that prompted the decision.

Gadia says many borrowers underestimate the legal responsibility that comes with signing a loan agreement.

"By signing a loan application as a co-borrower, joint borrower or guarantor, one is not merely helping the borrower emotionally. The person signing accepts financial responsibility. If the principal borrower delays EMI payments or defaults, the credit history of everyone responsible for the loan is likely to be affected."

Banks don't evaluate relationships.

They evaluate legal liability.

KNOW THE DIFFERENCE BEFORE YOU SIGN

Not every shared borrowing arrangement carries the same responsibility.

A co-borrower jointly applies for the loan and shares repayment responsibility.

A joint borrower generally shares both ownership of the asset and repayment liability.

A guarantor doesn't usually pay EMIs initially but becomes legally liable if the borrower defaults.

An authorised credit card user, on the other hand, can use the card but isn't legally responsible for repayment.

Understanding these distinctions before signing any document can prevent years of financial hardship.

WHY FAMILIES OFTEN WALK INTO THIS TRAP

According to Kundan Shahi, Founder of Zavo, most such situations arise within families because trust often replaces financial due diligence.

"Parents often become co-applicants for education loans. Spouses jointly apply for home loans. Siblings become guarantors for business loans. These decisions are usually made because of trust, not because of an assessment of financial risk. Unfortunately, lenders do not care about commitments. They only care about obligations."

For lenders, legal liability matters more than family relationships.

WHEN A FAMILY FAVOUR BECAME A FAMILY FALLOUT

If my professor friend's experience shows how a joint loan can cast a shadow years after a relationship ends, another story from my neighbourhood reveals how becoming a guarantor can come at an even heavier personal cost.

A neighbour once shared what happened to his father, who works in a bank.

Several years ago, he agreed to stand guarantee for his brother-in-law's car loan. It felt like a routine family favour. There was trust, goodwill and no reason to imagine anything could go wrong.

But the brother-in-law's business later suffered heavy losses. Soon, the EMIs stopped coming.

The bank, then, began contacting the guarantor instead.

At first, he repeatedly urged his brother-in-law to resume repayments. The response never changed—there was no money left.

Eventually, he had no choice but to repay the outstanding loan himself.

The financial burden was significant.

The emotional cost proved even greater.

A relationship that had been built over years slowly deteriorated over a loan that was never his in the first place.

It is a reminder that becoming a guarantor is never just a formality. It is a legal commitment that can outlive both the loan—and, sometimes, the relationship itself.

CAN YOU SIMPLY WALK AWAY?

Many people assume they can remove themselves as a guarantor or co-borrower after relationships change.

That's rarely the case.

According to Gadia, once you sign as a co-borrower or guarantor, your repayment responsibility continues unless the lender formally releases you. In the case of guarantors too, exiting generally requires lender approval, repayment of the loan or substitution with another acceptable guarantor.

A divorce decree, a family dispute or a broken relationship does not automatically end financial liability.

BEFORE YOU SAY YES, ASK YOURSELF THIS

Shahi believes every prospective co-borrower should pause before signing.

“Before you agree to co-sign a loan, ask yourself: if the borrower cannot repay the loan, can you afford to do it yourself? If the answer is no, it may be better to say no than to risk your credit score."

It's an uncomfortable question, but answering it honestly today could prevent years of financial distress tomorrow.

ONE SIGNATURE CAN CHANGE MORE THAN YOUR CREDIT SCORE

Money has an unusual way of testing relationships.

Sometimes it strengthens them. Sometimes it quietly breaks them.

For my professor friend, a joint loan continued to affect her long after her marriage had ended.

For my neighbour's father, standing guarantee for a relative meant not only repaying someone else's debt but also watching a family relationship fall apart.

Neither imagined that a signature made in good faith would carry such lasting consequences.

In the end, both stories point to the same truth: a signature is never just ink on paper. It is a promise that binds your financial future to someone else's decisions. And while credit scores can recover over time, relationships often don't.

"I had done everything right. So why was the bank treating me like a risky borrower?"

That question still haunts a friend of mine, a university professor who wishes to remain anonymous.

For years, she had been the kind of borrower banks love. Every credit card bill was paid on time. Every loan repayment was made without fail. She believed, like most of us do, that a good credit score was simply a reflection of personal financial discipline.

Then came a rude shock.

After separating from her husband, she decided to move on with life and applied for a personal loan. With a steady income and an impeccable repayment record, she expected the approval process to be routine.

It wasn't.

Banks either rejected her application or offered her a loan amount far below what she was eligible for.

Confused, she dug deeper.

That's when she discovered that her former husband had defaulted on multiple EMIs of the home loan they had once taken jointly.

Those missed payments on the joint loan had quietly affected her credit report, dragging down her credit score as well.

She had never missed an EMI or delayed a credit card payment herself. Yet her creditworthiness had taken a hit because of someone else's financial behaviour.

After months of discussions, paperwork and persuasion, she eventually secured a loan, but for a much smaller amount than she had originally sought, despite earning well enough to qualify for more.

Her experience reveals one of the least understood truths about borrowing: your credit score isn't always shaped only by your own financial discipline. Sometimes, it's shaped by someone else's decisions too.

YOUR SIGNATURE CARRIES MORE WEIGHT THAN YOU THINK

Many people believe that a credit score is influenced only by loans they personally borrow and repay.

Not quite.

According to Jyoti Prakash Gadia, Managing Director, Resurgent India Limited, becoming a co-borrower or guarantor legally ties your financial reputation to another person's repayment behaviour.

"It is often thought that an individual's credit score depends solely on one's loans, credit card usage and repayment behaviour. But that is not entirely true. If an individual acts as a co-borrower or guarantor to someone else's loan, even those loans may affect the individual's credit profile. Any default recorded against an individual can impact his or her future borrowing capacity."

In other words, your spotless repayment history may not be enough if you're legally connected to someone else's loan.

HELPING SOMEONE CAN TURN INTO A FINANCIAL LIABILITY

Few people think twice before signing loan documents for a loved one.

Parents become co-applicants on education loans. Couples jointly buy homes. Siblings stand guarantee for business loans. Friends step in during difficult times.

The intention is usually to help.

The legal consequences, however, can last much longer than the circumstances that prompted the decision.

Gadia says many borrowers underestimate the legal responsibility that comes with signing a loan agreement.

"By signing a loan application as a co-borrower, joint borrower or guarantor, one is not merely helping the borrower emotionally. The person signing accepts financial responsibility. If the principal borrower delays EMI payments or defaults, the credit history of everyone responsible for the loan is likely to be affected."

Banks don't evaluate relationships.

They evaluate legal liability.

KNOW THE DIFFERENCE BEFORE YOU SIGN

Not every shared borrowing arrangement carries the same responsibility.

A co-borrower jointly applies for the loan and shares repayment responsibility.

A joint borrower generally shares both ownership of the asset and repayment liability.

A guarantor doesn't usually pay EMIs initially but becomes legally liable if the borrower defaults.

An authorised credit card user, on the other hand, can use the card but isn't legally responsible for repayment.

Understanding these distinctions before signing any document can prevent years of financial hardship.

WHY FAMILIES OFTEN WALK INTO THIS TRAP

According to Kundan Shahi, Founder of Zavo, most such situations arise within families because trust often replaces financial due diligence.

"Parents often become co-applicants for education loans. Spouses jointly apply for home loans. Siblings become guarantors for business loans. These decisions are usually made because of trust, not because of an assessment of financial risk. Unfortunately, lenders do not care about commitments. They only care about obligations."

For lenders, legal liability matters more than family relationships.

WHEN A FAMILY FAVOUR BECAME A FAMILY FALLOUT

If my professor friend's experience shows how a joint loan can cast a shadow years after a relationship ends, another story from my neighbourhood reveals how becoming a guarantor can come at an even heavier personal cost.

A neighbour once shared what happened to his father, who works in a bank.

Several years ago, he agreed to stand guarantee for his brother-in-law's car loan. It felt like a routine family favour. There was trust, goodwill and no reason to imagine anything could go wrong.

But the brother-in-law's business later suffered heavy losses. Soon, the EMIs stopped coming.

The bank, then, began contacting the guarantor instead.

At first, he repeatedly urged his brother-in-law to resume repayments. The response never changed—there was no money left.

Eventually, he had no choice but to repay the outstanding loan himself.

The financial burden was significant.

The emotional cost proved even greater.

A relationship that had been built over years slowly deteriorated over a loan that was never his in the first place.

It is a reminder that becoming a guarantor is never just a formality. It is a legal commitment that can outlive both the loan—and, sometimes, the relationship itself.

CAN YOU SIMPLY WALK AWAY?

Many people assume they can remove themselves as a guarantor or co-borrower after relationships change.

That's rarely the case.

According to Gadia, once you sign as a co-borrower or guarantor, your repayment responsibility continues unless the lender formally releases you. In the case of guarantors too, exiting generally requires lender approval, repayment of the loan or substitution with another acceptable guarantor.

A divorce decree, a family dispute or a broken relationship does not automatically end financial liability.

BEFORE YOU SAY YES, ASK YOURSELF THIS

Shahi believes every prospective co-borrower should pause before signing.

“Before you agree to co-sign a loan, ask yourself: if the borrower cannot repay the loan, can you afford to do it yourself? If the answer is no, it may be better to say no than to risk your credit score."

It's an uncomfortable question, but answering it honestly today could prevent years of financial distress tomorrow.

ONE SIGNATURE CAN CHANGE MORE THAN YOUR CREDIT SCORE

Money has an unusual way of testing relationships.

Sometimes it strengthens them. Sometimes it quietly breaks them.

For my professor friend, a joint loan continued to affect her long after her marriage had ended.

For my neighbour's father, standing guarantee for a relative meant not only repaying someone else's debt but also watching a family relationship fall apart.

Neither imagined that a signature made in good faith would carry such lasting consequences.

In the end, both stories point to the same truth: a signature is never just ink on paper. It is a promise that binds your financial future to someone else's decisions. And while credit scores can recover over time, relationships often don't.